NEW DELHI: On April 6, 2026, the President of India gave assent to the Insolvency and Bankruptcy Code (Amendment) Act, 2026–No. 6 of 2026–and the legislation was published in the Gazette of India. A decade after the original IBC was enacted in 2016, Parliament has approved what practitioners call the most comprehensive rewrite of the code since its founding amendments.The Act amends 72 sections and inserts new frameworks: a creditor-initiated insolvency resolution process, a statutory group insolvency architecture, enabling provisions for cross-border insolvency and a new voluntary liquidation termination window. It also tightens admission timelines, rewrites the liquidation process and introduces stiff new penalties for misuse of the system.

Finance Minister Nirmala Sitharaman, piloting the Bill in Parliament, described the IBC as a law that responds to the growing needs of the economy and the government’s periodic review of stakeholder feedback.Sitharaman said, in the Rajya Sabha: “IBC was not brought with the intention of liquidating companies. It was brought in to address the stress that the companies are facing and give a resolution which will make them come back to some form and then attain the status that they were earlier running with quite a few guardrails.”She also placed on record that the IBC has contributed to the health of the Indian banking sector, noting: “One of the reasons why India’s banking sector has actually gotten better in itself is because of the way in which IBC has recovered assets and gone through the process and given back money to the banks.”

Why the Government moved the Amendment

The original IBC was enacted in 2016 to replace a broken insolvency regime built around the Sick Industrial Companies (Special Provisions) Act (SICA), where proceedings routinely stretched five to seven years, promoters retained control even through financial ruin and creditors had little practical recourse. The IBC marked a decisive shift: a time-bound process, creditor control, and a market-driven resolution.But a decade of experience exposed fresh cracks. The Parliamentary Standing Committee on Finance, in its report submitted in November 2025, catalogued the problems: the average time taken for closure of a Corporate Insolvency Resolution Process (CIRP) had reached 713 days–far beyond the statutory 330-day outer limit. NCLT benches were overloaded. Admission applications were taking months or years. Out of 1,326 avoidance-transaction applications filed for assets worth Rs 3.76 lakh crore, only about Rs 7,500 crore was recovered.

The Committee noted, in its report: “Protracted delays in proceedings, an excessive burden of litigation straining adjudicating authorities, contentious issues surrounding excessive haircuts for creditors, and the incomplete implementation of key frameworks, specifically the individual insolvency framework and the pre-packaged mechanism for MSMEs” were the primary systemic challenges.Sitharaman told Parliament the government aims to bring in expeditious admission of insolvency applications by limiting adjudication to the existence of default, greater reliance on information utilities and statutory timelines for adjudicatory authorities to reduce delays. She called strengthening the liquidation process through enhanced creditor oversight another key priority.Crucially, the minister addressed the criticism of low recovery rates directly, stating: “It was never intended to be a debt recovery tool. Recovery values are incidentally a by-product. The IBC process is market-driven. Recoveries are reflective of underlying asset quality and commercial viability of the distressed enterprise.”

What the numbers say: A decade of IBC

As of December 2025, the IBC has facilitated the resolution of 1,376 companies, enabling creditors to recover Rs 4.11 lakh crore. Financial creditors have seen recovery exceeding 34% of their total claims. This realization, the government noted, amounts to 171.54% of liquidation value– reflecting not a failure of the framework, but the distressed state of enterprises at entry.

Sitharaman told Parliament: “Banks have recovered a total of Rs 1,04,099 crore through various channels, and out of the total amount, the IBC channel alone contributed a significant Rs 54,528 crore, accounting for 52.3 per cent of the total recoveries.”The Standing Committee also noted, separately, that IBC had a significant deterrent effect–approximately Rs 13.94 lakh crore of debt had been resolved outside the formal process, with 1,154 companies withdrawn under Section 12A. Companies resolved through IBC saw a 76% average increase in sales post-resolution –figures drawn from an IIM Ahmedabad study of 1,194 resolved companies.

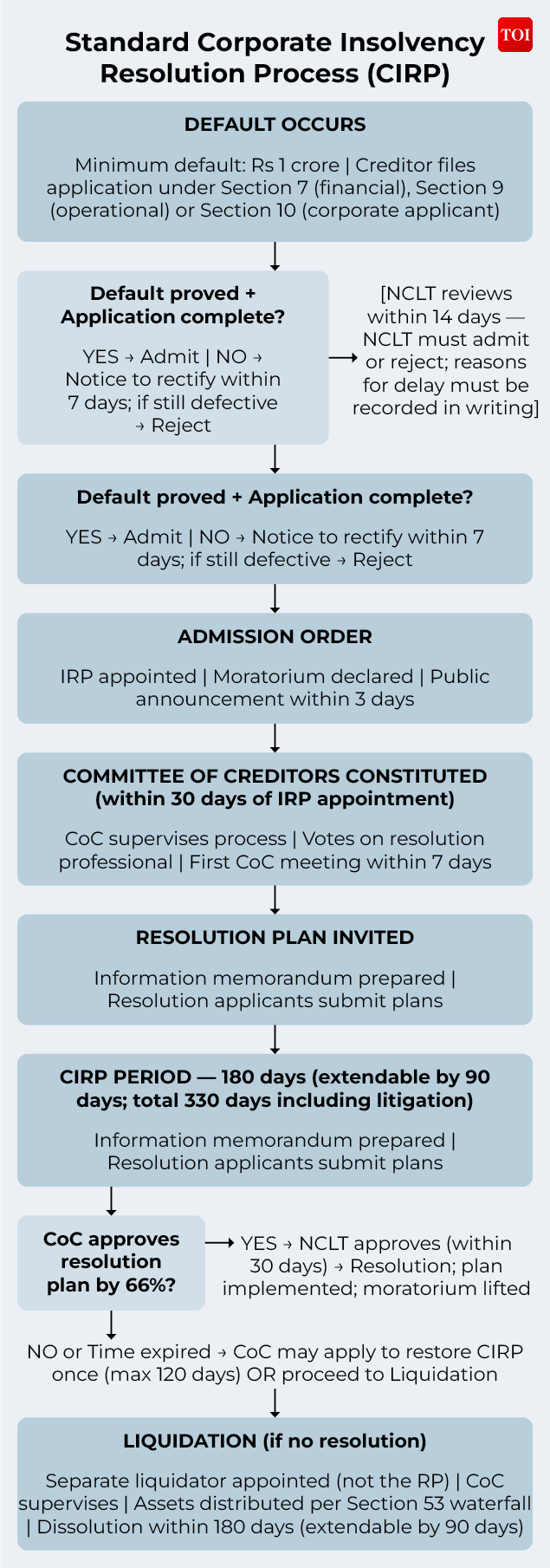

What changed: Faster admission, less room for delay

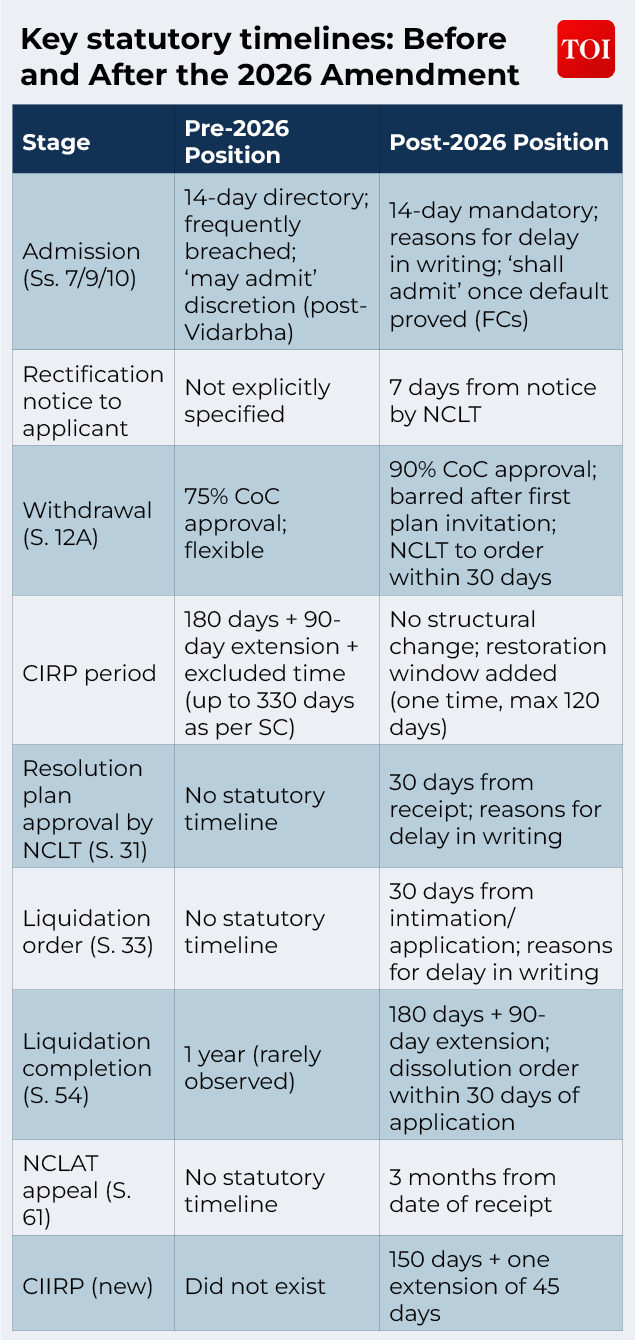

The most immediate change for litigants and creditors is at the admission stage. Under the amended Section 7(5), the National Company Law Tribunal (NCLT) must now admit or reject an insolvency application filed by a financial creditor within 14 days of receipt. If it fails to do so, it must record written reasons for the delay.Crucially, Explanation I to the amended Section 7(5) makes clear that once the statutory conditions — existence of default and completeness of the application — are satisfied, no other ground can be considered to reject the application. Similar 14-day mandates now apply under Sections 9 and 10 as well, covering operational creditors and corporate applicants respectively.

This provision is designed to close a gap created by the Supreme Court’s 2022 ruling in Vidarbha Industries Power Limited vs Axis Bank, where the use of the word “may” in the original text was interpreted to give NCLT discretionary power to refuse admission even after default was established.Mukesh Chand, Senior Counsel at Economic Laws Practice, explained the significance: “While there is no fundamental change in the role of the adjudicating authority, the amendment clarifies that in cases of financial creditors, the NCLT is to admit the application once default is proved. Earlier, this position was diluted due to the use of the word ‘may’ and the interpretation in Vidarbha Industries Power case.”The amendment also streamlines what counts as proof of default. Under amended Section 7(5), Explanation II now provides that a record of default furnished by a financial institution from an information utility shall be considered sufficient for the NCLT to ascertain the existence of default. This reduces the scope for prolonged preliminary hearings on the question of default.Neeha Nagpal, founding Partner of NM Law Chambers, captured the ground reality: “The intent is right. We have all seen how admission itself becomes a years-long battle, which completely defeats the purpose of the code. So mandating 14 days and asking tribunals to record reasons for delay, that is a good push. But the honest truth is: if you do not fix the NCLT’s capacity properly, this always stays on paper. The benches are overloaded. You can write the timeline into a statute, but if the infrastructure isn’t there, the judges will record a reason for delay and move on.”The Standing Committee had flagged the same concern, recommending urgently that additional NCLT benches be established and that the proposed Integrated Technology Platform (iPIE) for centralised case management be operationalised without delay.

The new path: Creditor-initiated insolvency resolution process

The most structurally novel addition in the 2026 amendment is Chapter IV-A–the Creditor-Initiated Insolvency Resolution Process (CIIRP). This is designed for a specific category of corporate debtors to be notified by the Central Government.Here is how the CIIRP works-A notified financial creditor, a bank or financial institution falling within a class to be specified by the government, identifies a corporate debtor in default. Before filing anything in court, the creditor must gather the support of financial creditors holding at least 51% of the debt. It must then give the corporate debtor a minimum 30-day notice to make a representation. After hearing that representation, the creditor again needs 51% approval from the financial creditor group before appointing a resolution professional.

Once the resolution professional is appointed, they publicly announce the commencement of the CIIRP. From that date, the corporate debtor has 30 days to file an objection before the NCLT if it disputes the default or the manner in which the process was triggered.The management of the corporate debtor remains with its board of directors–this is the ‘debtor-in-possession’ element–but the resolution professional attends all board and shareholder meetings and has the power to reject resolutions. A moratorium can be applied for with committee of creditors approval, but it is not automatic.The entire process must be completed within 150 days, extendable once by 45 days with 66% CoC approval. If no resolution plan is approved within that window, the process automatically converts to a full CIRP under Chapter II.Neeha Nagpal, Founding Partner of NM Law Chambers, noted “Asset-level resolution is pragmatic. We have had cases where the company as a whole is unsalvageable, but certain assets — like a plant, a portfolio, specific contracts — are completely viable. Earlier the framework did not give you clean tools to deal with that. Now this opens it up.”Commenting on the speed of proceedings, Jatin Kapoor, Partner Designate, S&A Law Offices told TOI, “These changes are expected to significantly improve the speed of insolvency proceedings, particularly at the admission stage, which has traditionally seen delays. The amendment simplifies the determination of default by recognizing records from information utilities as sufficient evidence, thereby reducing prolonged preliminary hearings” The Standing Committee, in its November 2025 report, had also recommended a framework for this kind of creditor-led, out-of-court initiation, noting that while the MSME Pre-Packaged Insolvency Resolution Process introduced in 2021 had seen very limited uptake — only 14 admitted applications by March 2025 — a creditor-initiated track designed for larger corporate debtors could work differently.

Rewriting the endgame: Reforms to liquidation

The 2026 amendment significantly reshapes the liquidation framework under Chapter III, addressing long-standing concerns around delays, conflicts of interest, and limited creditor oversight.A key structural change is the clear separation between the resolution professional and the liquidator. Under the amended Section 34(4), the resolution professional who conducted the CIRP is barred from being appointed as the liquidator for the same corporate debtor. Instead, the Insolvency and Bankruptcy Board of India must recommend a different insolvency professional within ten days of a reference from the Adjudicating Authority.The role of the committee of creditors has also been expanded. Under Section 21(11), the CoC continues during liquidation and supervises the conduct of the liquidator. It is further empowered, under the newly inserted Section 34A, to replace the liquidator with a 66% voting share.Timelines have been tightened, with the liquidator required to complete the process and apply for dissolution within 180 days, extendable by up to 90 days. The Adjudicating Authority must then pass a dissolution order within 30 days.The amendment also introduces a more flexible pathway for closure. The CoC may resolve to dissolve the corporate debtor, subject to prescribed conditions and approval by the Adjudicating Authority. While this enables a more streamlined exit in appropriate cases, it does not entirely bypass the need for asset realisation and distribution where assets remain.Sonam Chandwani, Managing Partner of KS Legal & Associates, observed a broader strategic shift: “The amendments push the Code further towards a recovery-driven model by expressly enabling asset-level resolution and by pulling guarantor assets into the process, which should in principle improve value realisation where enterprise value has already collapsed. At the same time, this marks a shift away from the original design of preserving the corporate debtor as a going concern, and in practice may lead to value extraction rather than value preservation.“

Protecting dissenting creditors: A Long-pending fix

One of the sharpest and most debated technical changes in the 2026 amendment concerns how financial creditors who vote against a resolution plan must be treated.Under the new Section 30(2)(ba) of the principal Act, a resolution plan must now provide for payment to dissenting financial creditors in an amount that is not less than the lower of: what they would receive in liquidation under Section 53, or what they would receive if the plan’s distributable amount were allocated in the Section 53 waterfall order.In plain terms, a dissenting financial creditor cannot be paid less than they would get in the worst-case scenario–liquidation. The Explanation to the new clause clarifies that this distribution shall be “fair and equitable” to such creditors.This provision responds to a specific problem: under the original IBC, there were instances where resolution plans approved by a 66% voting share left dissenting creditors with amounts below their expected liquidation recovery. The amendment puts a statutory floor on how badly a minority creditor can be treated by the majority.Mukesh Chand, partner at Economic Laws Practice, added a caution: “With every amendment to the Code and regulations, the focus has increasingly shifted towards recovery, with a clear tilt in favour of financial creditors. FCs not only control the outcome but also dominate recovery, and the Code is often being used as a recovery tool, with even units facing temporary stress getting pushed into insolvency. The need is to shift the focus from recovery to revival and preservation of industry.“

After approval: Implementing resolution plans

The amendment addresses a complaint from resolution applicants: that approved resolution plans can be stalled by pending regulatory clearances, government permits or legacy proceedings.Under newly inserted Section 31(5), once a resolution plan has been approved by the NCLT, no licence, permit, registration, quota, concession or clearance granted by any central or state government body shall be suspended or terminated during its remaining validity period— provided the corporate debtor or the new owner complies with the obligations attached to those grants.Under Section 31(6), all prior claims against the corporate debtor and its assets are extinguished from the date of plan approval. No proceedings can be continued or initiated on the basis of such claims, including assessment proceedings. However, the Explanations make clear that this clean-slate protection does not extend to promoters, guarantors or persons with joint liability–they remain exposed.Earlier, the Standing Committee had recommended that a transparent online mechanism be created for issuing ‘no dues’ certificates and statutory clearances immediately upon completion of a resolution plan, so that revitalised companies truly start fresh.

Pulling guarantor assets into the process

A new Section 28A allows a creditor who has taken possession of an asset of a personal or corporate guarantor –by enforcing its security interest to permit the transfer of that asset as part of the corporate debtor’s insolvency resolution, with CoC approval. Where the corporate guarantor is itself undergoing insolvency, the transfer needs approval from the guarantor’s own CoC by at least 66% voting share. Where the personal guarantor is in insolvency proceedings, approval requires more than 75% in value of that guarantor’s creditors.Vikash Kumar, Associate at Saikrishna & Associates, flagged a connected reform on the definition of security interest: “The amendment to Section 3(31) clarifies that a security interest will be recognised only where it is created pursuant to an agreement or arrangement involving the act of two or more parties. Crucially, it expressly excludes security interests that arise solely by operation of law. This clarification appears to directly address the controversy stemming from judgments such as Greater Noida Industrial Development Authority vs Prabhjit Singh Soni, where statutory authorities were treated as secured creditors.“The practical significance, as Kumar noted, is that authorities like NOIDA and GNIDA — which had claimed secured-creditor status on the basis of statutory charges over land or project assets are now outside the definition of secured creditor. This matters particularly for homebuyers in real estate insolvencies, who had been pushed below these authorities in the distribution waterfall.

Group insolvency and cross-border frameworks

Two other enabling frameworks have been inserted into the IBC’s statutory structure: group insolvency and cross-border insolvency.Chapter V-A, Section 59A, empowers the Central Government to prescribe rules for conducting insolvency proceedings where two or more corporate debtors form part of a corporate group. The rules may provide for a common NCLT bench, coordination between committees of creditors, a common insolvency professional, and binding cross-entity coordination agreements. A group is defined in the Act as two or more corporate debtors interconnected by control or significant ownership, with significant ownership meaning 26% or more voting rights.Section 240C introduces an enabling framework for cross-border insolvency, empowering the Central Government to prescribe rules for the recognition of foreign insolvency proceedings, granting relief, judicial cooperation and coordination. The Standing Committee had recommended selective adoption of the UNCITRAL Model Law on Cross-Border Insolvency, with modifications suited to India’s financial and legal framework.Both frameworks currently vest rule-making power in the Central Government and do not have immediate operational effect. Rules will need to be notified before either framework becomes functional. The Standing Committee’s report noted that “the establishment of cross-border insolvency is the need of the hour in a developing nation like India” given the increasing number of corporate entities operating internationally with assets spread across multiple jurisdictions.

Stiffer penalties, new enforcement tools

The 2026 amendment strengthens the penalty framework under the IBC, reflecting concerns around frivolous litigation, non-compliance, and delays in the insolvency process. While the Parliamentary Standing Committee had recommended more stringent deterrents, including an upfront deposit requirement for appeals by unsuccessful resolution applicants, this particular proposal has not been incorporated into the statute.The newly inserted Section 64A introduces a specific penalty for initiating frivolous or vexatious proceedings before the Adjudicating Authority, with fines ranging from ₹1 lakh to ₹2 crore. A corresponding provision, Section 183A, applies similar penalties within the individual insolvency framework.Additional provisions, including Sections 67B and 67C, expand the scope for penal action by empowering the Adjudicating Authority to impose monetary penalties in cases such as violations of the moratorium, breaches of approved resolution plans, and misconduct in the filing of applications.The amendment also revises Section 235A, the general penalty provision, to enhance the deterrent effect of non-compliance. It provides for significantly higher penalties, including amounts linked to the loss caused or unlawful gain, subject to prescribed limits where such amounts cannot be quantified.Taken together, these changes signal a shift towards a more enforcement-driven insolvency regime, aimed at discouraging abuse of process and ensuring greater discipline among stakeholders.

Tighter withdrawal rules and avoidance transactions

Section 12A, which governs withdrawal of admitted applications, has been rewritten. Withdrawal now requires a 90% voting share of the CoC–up from the previous threshold–and the NCLT must pass an order on the withdrawal application within 30 days. Crucially, withdrawal is completely barred after the first invitation for resolution plan submissions has been issued — preventing last-minute exits designed to gain tactical leverage.On avoidance transactions–transactions that defraud or disadvantage creditors through preferential payments, undervalued deals or extortionate credit arrangements–the amendment strengthens the filing and continuation mechanism. A new Section 26 makes clear that proceedings in respect of avoidance transactions or fraudulent trading continue independently of the CIRP or liquidation process: completing the main process does not kill the avoidance proceedings.Under the revised Section 47, creditors who believe an avoidance transaction has occurred but has not been reported by the resolution professional or liquidator can themselves apply to the NCLT. If the NCLT finds the RP failed to act despite having sufficient information, it must direct IBBI to initiate disciplinary proceedings against that professional.

The big picture: What experts are watching

Sonam Chandwani of KS Legal & Associates offered a structural caution: “On admission, a more default-driven approach may improve predictability, but reduced judicial scrutiny can shift the burden of dispute resolution to later stages such as plan approval and distribution, where litigation is often more value-destructive. It also raises a broader concern of whether the Code is gradually moving from a resolution statute to a debt enforcement mechanism, which was never its original legislative intent.““Overall, the amendments do improve flexibility and may deliver better outcomes in straightforward cases, but in complex, multi stakeholder insolvencies they are equally likely to redistribute litigation across stages and stakeholders. The effectiveness of these changes will ultimately depend on how tightly adjudicating authorities control process discipline and resist expanding the scope of intervention.” She added. “On creditor priority, I’d say watch this space very carefully. Anytime you shift the waterfall, you risk sending signals to lenders. If secured creditors feel their position is less certain, that, you know, affects the credit behavior downstream. So the policy intent may be sound, but implementation needs to be very precise and very consistent. And judicial interpretation needs to follow through. So, that’s where it could either work really well or create new uncertainty.” says Neeha Nagpal, Founding Partner of NM Law Chambers. Vikash Kumar, noted the execution risk: “The amendment is likely to improve recovery outcomes by introducing greater flexibility and clarity. By allowing asset-level resolution, it enables targeted sales that can maximise value rather than relying solely on whole-business resolutions. But without adequate safeguards, they may also lead to increased litigation and delays, which have historically undermined recovery timelines.“The Standing Committee, in its conclusion, stated that the primary issues remaining are “protracted delays stemming from inadequate judicial infrastructure, the uncertainty regarding the finality of resolution plans (exacerbated by judicial reversals and the statutory overlap with PMLA), and a lack of accountability among resolution professionals, whose role is critical as they drive the success of this credit-driven law.“The Committee called for immediate action on judicial capacity: new NCLT benches, filling of vacant positions, and operationalising the long-pending Insolvency and Bankruptcy Fund under Section 224, which, despite being requested by IBBI since 2019, had not been operationalised as of the report’s submission.